Does Manufacturing Matter? Yes It Does. Here’s Why.

Last month, author, academic and Substack blogger Chris Miller asked the question “Does Manufacturing Matter?” It’s a question on many people’s minds: does the U.S. need to regain its onetime manufacturing prowess? And even if it does, can it? And how could it do so?

Miller, author of the excellent book Chip Wars, said he wasn’t sure if manufacturing matters to the U.S. But he made the very good point that Americans are not sufficiently aware of the trade-offs involved in developing a national strategy to support manufacturing growth.

Here I will explain that manufacturing does matter, why, and how we begin to go about rebuilding key parts of the manufacturing sector. Manufacturing matters not just on national security grounds, which most people understand, but on economic grounds. The relative decline in manufacturing explains a large part of the slowdown in U.S. economic growth since 2000 and the rise in inequality.

The starting point for any such analysis should be the U.S. trade deficit. When we get the data for December 2025, the U.S. will have run a trade deficit for 50 consecutive years. There is no record of any nation in history having run a trade deficit for so many years.

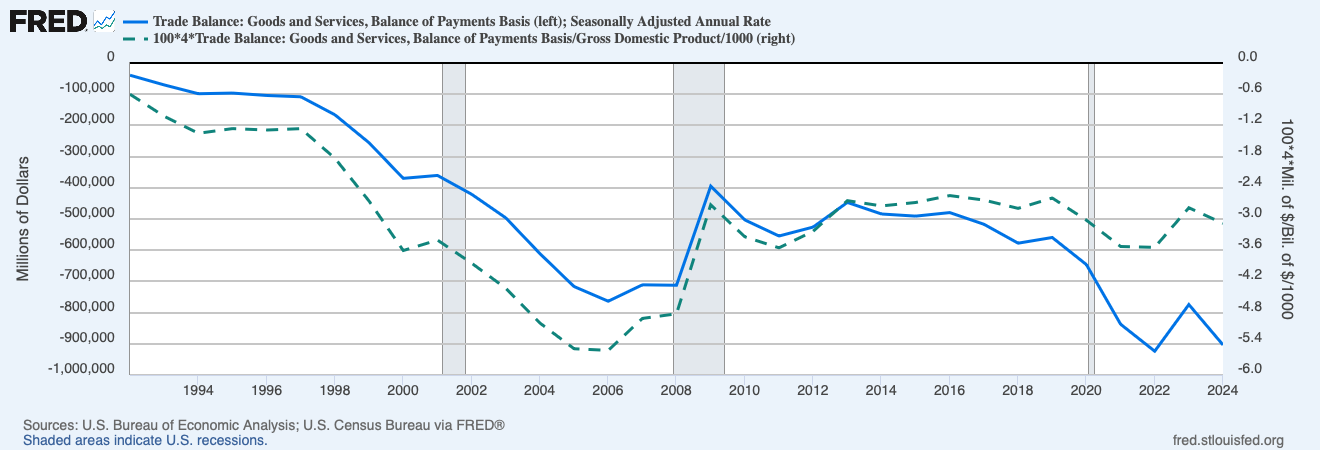

As Figure 1 shows, our trade deficits (blue line) have grown steadily larger, except for a brief respite when the 2008 recession choked down imports. They have hovered at around 3% of GDP for many years (green line, right-hand axis). In 2024, the deficit hit $903.5 billion. When we get November and December 2025 data, we will likely be looking at a 2025 (goods and services) deficit of some $850 billion, slightly better than 2024 but still the third-worst trade deficit in U.S. and world recorded history. The deficit on goods trade will be larger, around $1.2 trillion.

Figure 1. U.S. trade deficit in 2024 was $903.5 billion.

One of the few laws in economics that actually holds is Stein’s Law: if something cannot go on forever, then one day it will stop. The only way a nation can run a trade deficit is by foreigners lending it the money to buy imports. Our net international investment position is currently running at minus $26 trillion. In other words, net of all our international assets, we owe $26 trillion to the rest of the world. That’s about $80,000 per American.

At some point foreigners will grow tired of lending us close to a trillion dollars a year and they will stop. When that happens, we can expect the dollar to fall very substantially, import costs to rise substantially, the federal government to encounter difficulties in funding the trillion-dollar-plus federal deficit, and interest rates to rise. In other words, a crisis.

As a rich nation, the U.S. had higher costs than most of its competitors throughout the 20th century. We did not prioritize exports or balanced trade. We have been a nation that got rich by selling products to our own consumers and getting our banks to lend money generously to our producers and consumers to build and buy those goods, amplifying the momentum of our consumer-led economy. From the 1970s on, we embraced the idea that globalization would drive us to greater efficiency. We made a foolish mistake. U.S. workers simply refused to accept the pay cuts that globalization implied. In most cases, U.S. employers did not even dare to ask them for pay cuts on such a scale. (For example, Mexican auto workers earn some 80% less than U.S. auto workers.) American corporations found the easiest solution was to offshore production.

Imports surged and the trade deficit exploded. Politicians, faced with the choice of doing something about U.S. competitiveness or using borrowed foreign money to keep funding the trade deficit, took the cash. Politicians’ priority has always been to keep the economy and consumer spending churning upwards to help win the next election. Anglo-Saxon democracy, with its two-party systems, is structured to focus attention on the short-term, i.e. the next election. That’s why the U.S. and the U.K. accounted for about 86% of the world’s trade deficits, by IMF figures.

Figure 2 shows the current structure of U.S. goods imports. When the market finally forces us to balance trade, we will need to find a way to close this nearly $1 trillion gap. Since it is hard to raise exports quickly, most of the savings will have to be found by cutting imports. Americans regard most of the categories of goods in Figure 2 as essential, so import reduction will not be easy. Since manufactured goods account for some 75% of our trade (the rest is services and agricultural goods), it will be manufactured goods where we will need to reduce imports or increase exports.

Figure 2. US goods imports in 2024 of $3.2 billion were led by motor vehicles, pharma, and IT equipment.

Profits, Pay, and Prosperity

In my previous blog post, I documented the evidence that manufacturing jobs currently pay some 12.7% better than the average job in the U.S., and what I called economically advantageous manufacturing sectors pay 36% better than the average U.S. job.

The fundamental reason why manufacturing jobs tend to pay well is that manufacturing companies succeed through innovation. Innovation generates product differentiation and market dominance by a small number of competitors, i.e. oligopolistic competition. Oligopoly and differentiation lead to greater profitability. Profitability and high employee earnings are positively correlated. That’s why computer industry earnings show up as the most highly paid manufacturing sector.

The link between high profits and high worker earnings is counterintuitive for many people, because they think of a company as having a fixed pool of profit and higher worker pay must arithmetically diminish profits. However, when you look across companies and industries, higher profit goes hand in hand with higher employee pay. Dozens of studies[1] have found this to be true.

The profit-pay relationship is downplayed (and often denied) by two prominent groups: union officials and economists. Union officials play up their own importance by pretending that businesses are hiding large sums of profit and unionization is the best way for workers to claim a larger share of that cash. Unions do in fact increase worker pay, but only at the margin and only where the profit is already there to be claimed, or fought for. Economists, on the other hand, resist the idea that worker pay is dependent on profitability because the basic economic model (general equilibrium and output maximization) taught at all universities rests on an assumption that each worker is paid according to his or her skill level. A model where worker pay varies with profit, company, or industry, disturbs the beautiful harmony of standard economic models. (It also suggests that nations should compete with each other to claim the best, i.e. most profitable, industries, instead of cooperate and engage in the so-called “international rules-based order.”)

The other major strategic advantage of manufacturing is that it typically employs large numbers of people, ranging from those without specialized skills or education to the highly educated. This has made it an excellent way to distribute prosperity to thousands of workers and their families.

In the years before 1945, the U.S. could leave it to the market and individual businessmen to search out and build the most profitable businesses. But after 1945, shipping costs collapsed and it became much easier to manufacture in one place and ship products to multiple countries around the world. The invention of the container ship in the 1950s probably did more to encourage world trade than so-called free trade agreements. Beginning in the 1960s, countries like Japan and later Korea and China could target the most profitable U.S. industries, manufacturing products in their countries for the U.S. market. This undermined U.S. manufacturing and the incomes of millions of workers, especially less-educated and less-skilled workers.

Productivity

Above we talked about comparative earnings levels across companies and industries. But over time, i.e. ten or twenty years or more, the most important force in raising incomes is increasing labor productivity.

Manufacturing industry has a long history of increasing labor productivity. Service industries rarely offer the same opportunities for increasing productivity. This is why manufacturing has been at the heart of most of the industrial revolutions in the U.S. and other countries over the last 500 years.

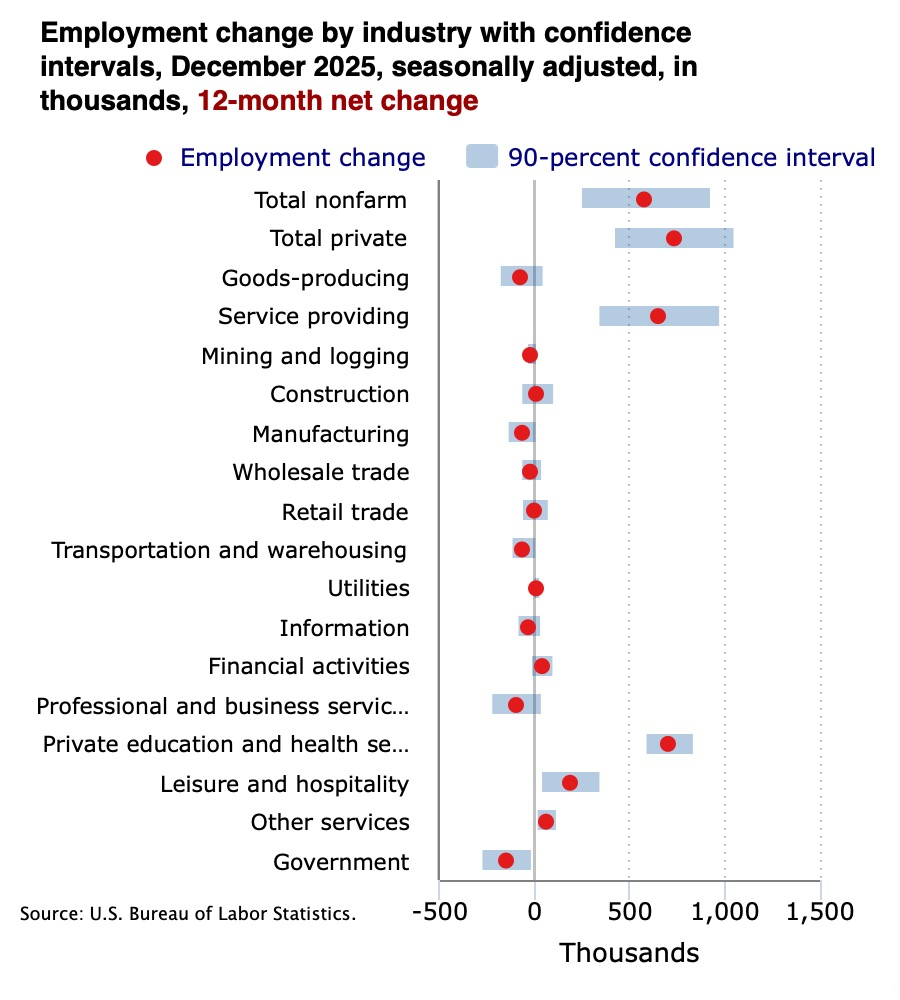

Figure 3 highlights the problem. The chart, recently published by the Bureau of Labor Statistics, shows that, of the broad industry groups in the chart (from “Mining and Logging” down to “Government”) the only two that showed substantial employee growth over the year 2025 were “Private Education and Health Services” and “Leisure and Hospitality.” While all these services are essential, none of them are capable of generating sustained productivity growth of the kind that can translate into generalized prosperity. For example, health care capabilities are improving steadily and one could measure “health productivity” in growing life expectancy. But in economic terms, health care is absorbing an ever-larger share of spending, now around 18% of GDP, generates more low-paid jobs than high-paid, and shows little if any improvement in economic productivity. In fact, spending on health care, whether through taxes or insurance payments, acts as a burden on household incomes, adding to Americans’ feeling of a higher cost of living.

Figure 3. A BLS chart shows that 2025 employment growth occurred in two low-productivity-growth sectors.

In the blog by Chris Miller cited at the start of this post, he argues that manufacturing is too small to move the needle for the U.S. economy. It’s true that it is today only some 10% of U.S. GDP and 8% of U.S. employment. The Economist magazine recently made a similar argument for Germany, suggesting that as German industrial companies succumb to Chinese competition, Germany should rebuild its service industries instead. But this is to ignore the dynamic effects of industrial growth.

All economic growth stories are based on industries that start relatively small and grow over time. The revenue, profit, investment, and earnings of all workers in that industry flow to other industries within the nation, generating a dynamic effect over time that raises the prosperity of the entire nation.

This is the effect we need in the U.S. However, it should not be scattershot. Because the initial costs of such a program are significant, whether they take the form of tariffs, subsidies or other measures, they must be focused on the industries that can generate the most bang for the buck. They must also take national security needs into account. We cannot know for certain what industries will turn out to be best in ten or twenty years time. But we must make our bets. National security investments may cost us money. But investments made in industries that will grow and generate profit, investment, higher pay, and growth, will pay off.

One thing I learned in my years in the technology industry is that every company needs a plan. That goes for countries too. We must make bets on specific industries. We must also be careful to maintain vigorous competition within those industries. No giveaways. The saying every year as Silicon Valley tech companies make their annual plans is: “Those who fail to plan, plan to fail.”

[1] Two articles that surveyed the huge literature devoted to the pay-profit correlation are: Jeffrey Ferry, Free Trade Theory and Reality: How Economists Have Ignored Their Own Evidence for 100 Years, Real-World Economic Review, Sept. 22, 2022 and David Card, Ana Rute Cardoso, Jörg Heining, and Patrick Kline, Firms and Labor Market Inequality: Evidence and Some Theory, NBER Working Paper 22850, November 2016. The Card paper estimated that a 10% increase in corporate profitability per worker led to a 1% increase in pay. So if company A earned five times the profit per worker as company B, it would pay its average employee 50% higher wages. Card won the Nobel Prize in Economics in 2021.

Why the USA has lost its manufacturing is a key question for figuring out how to get it back. There is no denying that lower shipping costs encouraged US manufacturers to relocate manufacturing plants to source lower-cost labor. But is that all? Is it the reason RCA and many other American companies lost radio, TV, and consumer electronics manufacturing busienss? Similarly, is it for this reason that Ratheon lost Miccrowave oven and Kodak lost film manufacturing? Unless we find clear answers to these questions, the USA will keep struggling to figure out how to get manufacturing back and create high-paying jobs by adding high value.